:max_bytes(150000):strip_icc():format(jpeg)/uBAhh-30-year-refinance-rates-by-state-dec-26-2024-5dbde10c83a2412599ad15a5f2b0fa25.png)

Editor’s Note: Investopedia did not publish daily mortgage rate news on Wednesday, Dec. 25, in observance of Christmas Day. We are, therefore, reporting today on Tuesday’s rate averages.

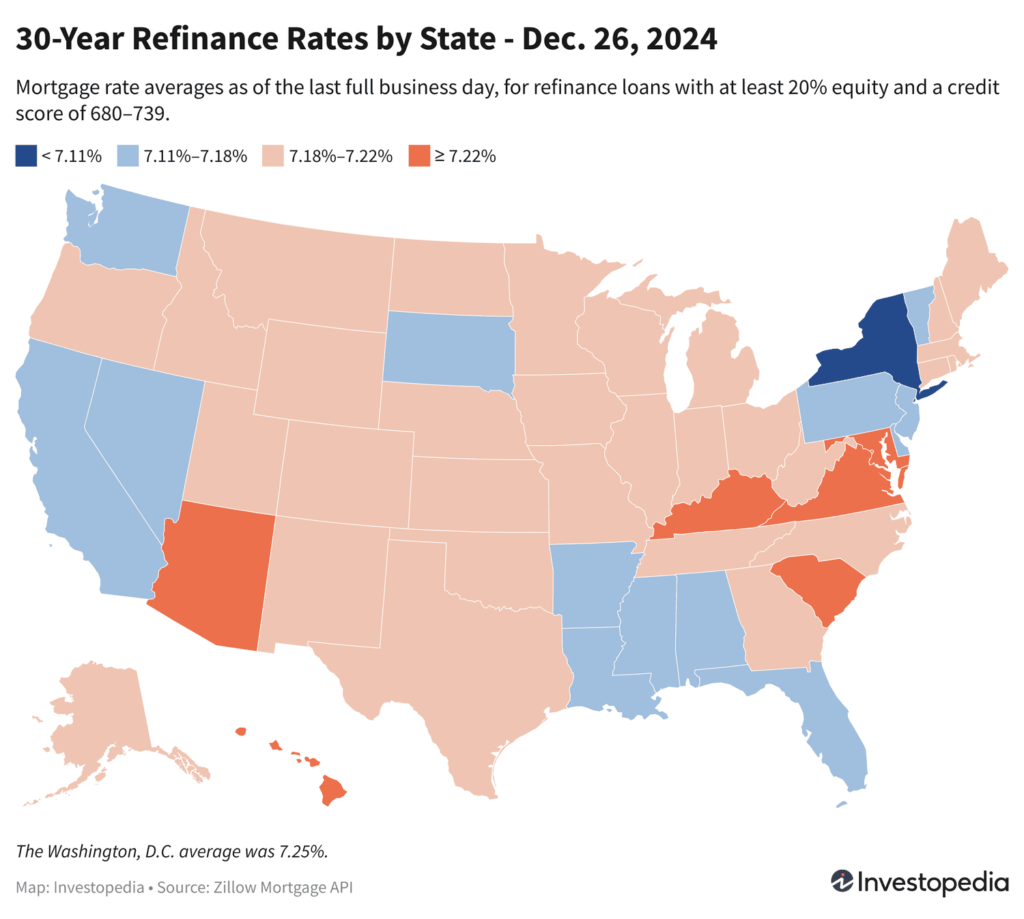

The states with the cheapest 30-year mortgage refinance rates Tuesday were New York, New Jersey, Louisiana, Pennsylvania, Alabama, Delaware, and Florida. The seven states registered 30-year refi averages between 6.93% and 7.15%.

Meanwhile, the states with the highest Tuesday refinance rates were Washington, D.C., Virginia, South Carolina, Hawaii, Arizona, Maryland, and Kentucky. The range of 30-year refi averages for these states was 7.22% to 7.25%.

Mortgage refinance rates vary by the state where they originate. Different lenders operate in different regions, and rates can be influenced by state-level variations in credit score, average loan size, and regulations. Lenders also have varying risk management strategies that influence the rates they offer.

Since rates vary widely across lenders, it’s always smart to shop around for your best mortgage option and compare rates regularly, no matter the type of home loan you seek.

Important

The rates we publish won’t compare directly with teaser rates you see advertised online since those rates are cherry-picked as the most attractive vs. the averages you see here. Teaser rates may involve paying points in advance or may be based on a hypothetical borrower with an ultra-high credit score or for a smaller-than-typical loan. The rate you ultimately secure will be based on factors like your credit score, income, and more, so it can vary from the averages you see here.

National Mortgage Refinance Rate Averages

The national average for 30-year refinance mortgages added 7 basis points Tuesday, taking the average to 7.19%—a five-month high. The current average sits almost 1.2 percentage points above mid-September when it sank to 6.01%—its cheapest level in 19 months.

| National Averages of Lenders’ Best Mortgage Rates | |

|---|---|

| Loan Type | Refinance Rate Average |

| 30-Year Fixed | 7.19% |

| FHA 30-Year Fixed | 6.29% |

| 15-Year Fixed | 6.09% |

| Jumbo 30-Year Fixed | 7.13% |

| 5/6 ARM | 6.85% |

| Provided via the Zillow Mortgage API | |

Calculate monthly payments for different loan scenarios with our Mortgage Calculator.

What Causes Mortgage Rates to Rise or Fall?

Mortgage rates are determined by a complex interaction of macroeconomic and industry factors, such as:

Because any number of these can cause fluctuations simultaneously, it’s generally difficult to attribute any change to any one factor.

Macroeconomic factors kept the mortgage market relatively low for much of 2021. In particular, the Federal Reserve had been buying billions of dollars of bonds in response to the pandemic’s economic pressures. This bond-buying policy is a major influencer of mortgage rates.

But starting in November 2021, the Fed began tapering its bond purchases downward, making sizable monthly reductions until reaching net zero in March 2022.

Between that time and July 2023, the Fed aggressively raised the federal funds rate to fight decades-high inflation. While the fed funds rate can influence mortgage rates, it doesn’t directly do so. In fact, the fed funds rate and mortgage rates can move in opposite directions.

But given the historic speed and magnitude of the Fed’s 2022 and 2023 rate increases—raising the benchmark rate 5.25 percentage points over 16 months—even the indirect influence of the fed funds rate has resulted in a dramatic upward impact on mortgage rates over the last two years.

The Fed maintained the federal funds rate at its peak level for almost 14 months, beginning in July 2023. But on Sept. 18, the central bank announced a first rate cut of 0.50 percentage points, and then followed that with quarter-point reductions on Nov. 7 and Dec. 18.

However, the Fed’s policy committee cautioned at its meeting last week that, due to stubborn inflation, further rate cuts may be fewer and farther between. This scaled-back forecast for 2025 reductions pushed 10-year Treasury yields higher, which in turn triggered a mortgage rate rise.

How We Track Mortgage Rates

The national and state averages cited above are provided as is via the Zillow Mortgage API, assuming a loan-to-value (LTV) ratio of 80% (i.e., a down payment of at least 20%) and an applicant credit score in the 680–739 range. The resulting rates represent what borrowers should expect when receiving quotes from lenders based on their qualifications, which may vary from advertised teaser rates. © Zillow, Inc., 2024. Use is subject to the Zillow Terms of Use.